I II and III b. Vouching and verification of all the purchases and disposals of the investments.

The Completeness Assertion And Purchase Cutoffs Youtube

1

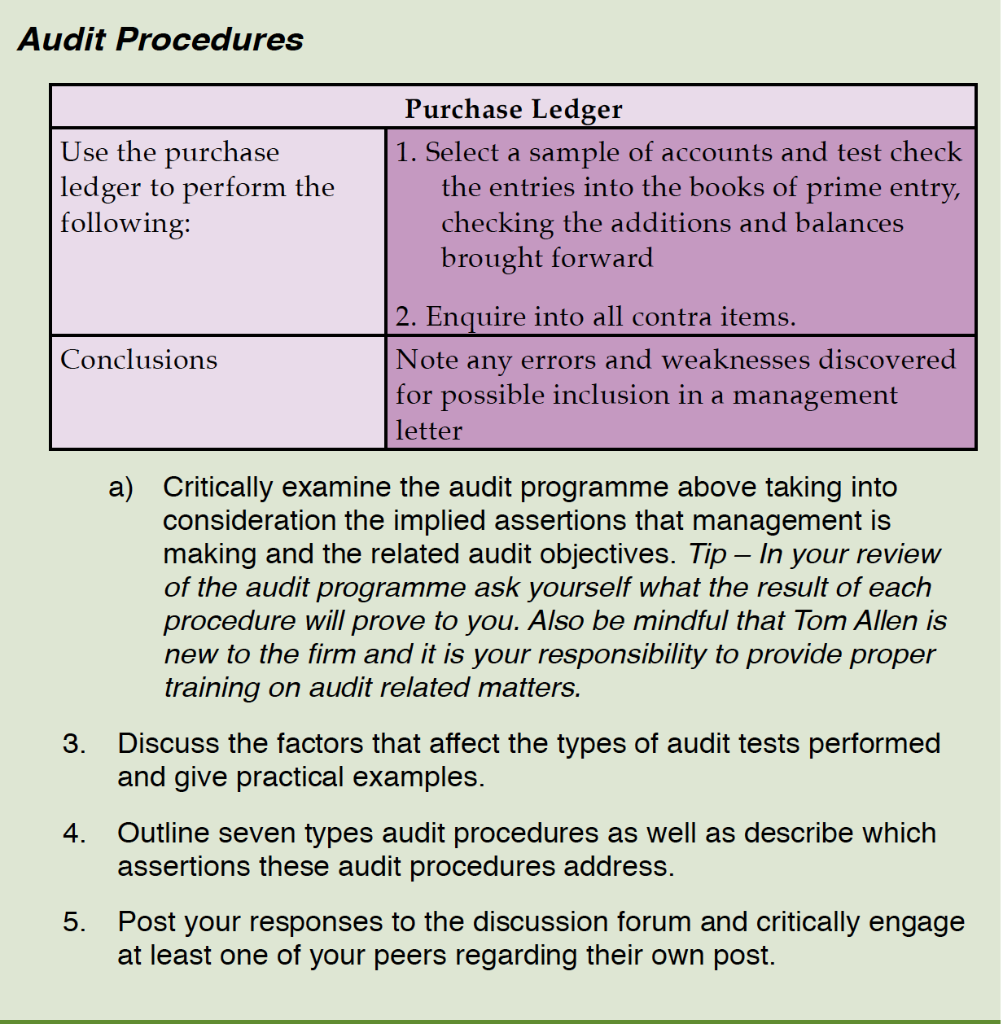

Audit Procedures Use The Purchase Ledger To Perform Chegg Com

A schedule of time spent on the engagement by each individual auditor.

Audit assertions for purchases. So my RMM for these assertions is usually moderate to high. The auditor then assesses control risk for the relevant assertions embodied in the account balance. Today we talk about auditing plant property and equipment or capital assets if you work with governments.

143 when management has used the work of a specialist in developing accounting estimates as well as other amendments to enhance guidance about evaluating the work of the managements specialist. Assertions about account balances at the period end. ICQ Internal Control QuestionnaireSales Transaction Processing Assertions and Questions Yes No NA Comments Occurrence assertion.

In the audit of investments the inherent risk of investments involves more on the existence and valuation of their balances. Audit procedures designed and performed by the auditor should clearly document the audit objective that they intend to achieve in terms of assertions relating to a specific class of transactions account balance or disclosure the actual work performed the results obtained their evaluation and a conclusion as to whether the audit evidence obtained is sufficient and appropriate to verify or. Audit procedures for receivables.

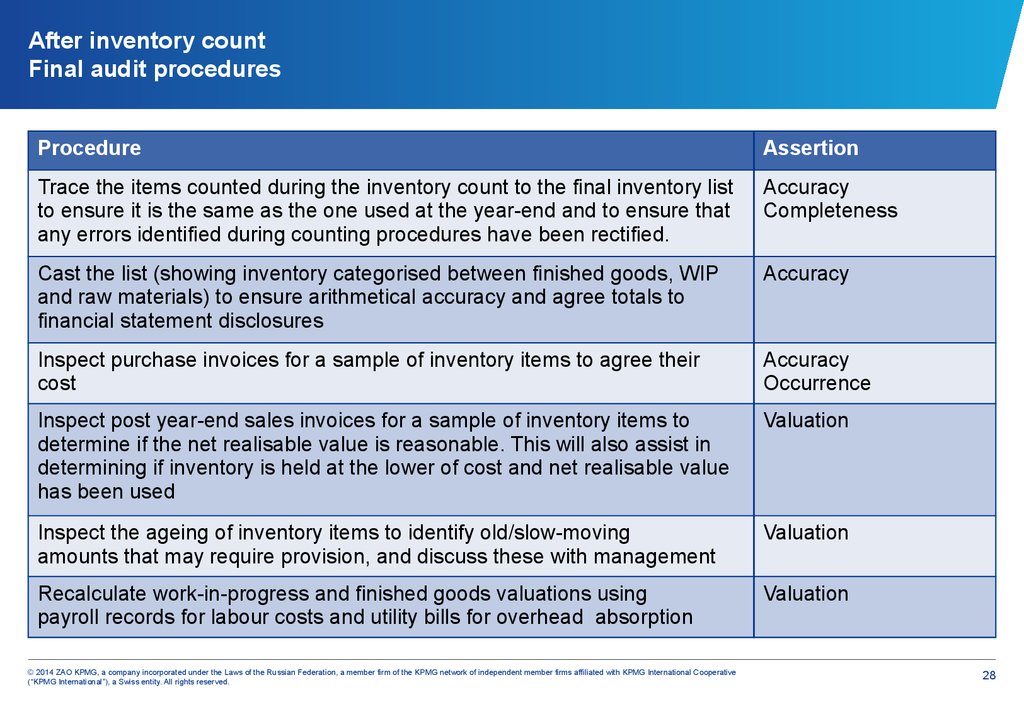

A for most assertions analytical procedures are considered less effective than tests of details so analytical procedures are used as a supplement to tests of details. In the audit process of inventory physical inventory count may be the most important part of the inventory audit. This refers to the possibility that an organizations internal controls may not detect or prevent compliance deficiencies.

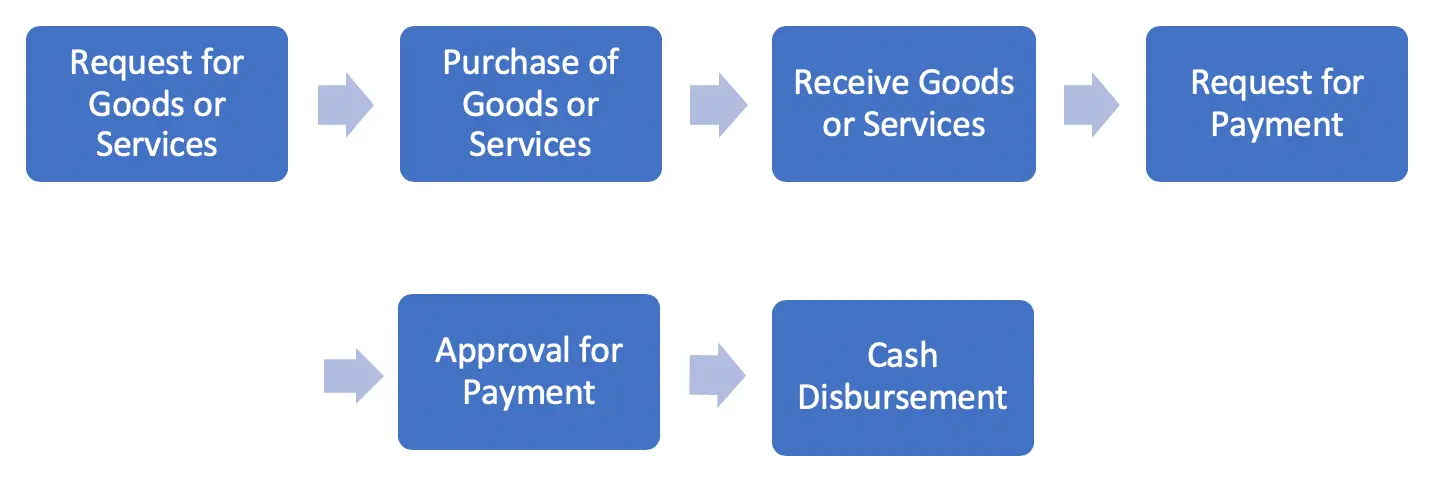

Determining Detection Risk Detection risk for payables assertions is affected by inherent and control risk factors related to both the purchases transactions and cash disbursements transactions classes. Audit of Property Plant and Equipment and the Related Depreciation. In planning and performing an audit an auditor considers these assertions in the context of their relationship to a specific account balance or class of transactions63.

As auditors we usually audit investments that the client has on their financial statements by testing various audit assertions including existence completeness valuation and rights and obligations. After all its difficult to steal land or a building. 1 The auditor uses his professional judgment to determine the allowable audit risk after considering factors such as those discussed in.

But the risk is often low to moderate. Assertions about classes of transactions and events and related disclosures for the period under audit i Occurrence the transactions and events that have been recorded or disclosed have occurred and. So the dollar amount can be high but the risk low.

Key Assertions of the Audit of Inventory. The assertions that concern me the most are completeness occurrence and cutoff. Audit Evidence and Audit Programs.

C analytical procedures are often the costliest to perform. The ledger accounts of a business are the main source of information used to prepare the financial statementsHowever if a business were to update their ledgers each time a transaction occurred the ledger accounts would quickly become cluttered and errors might be made. The term property plant and equipment fixed assets include all tangible assets with a service life of more than one year that are used in the operation of the business and are not acquired for the purpose of resale.

Books of prime entry Introduction. Analytical Procedures consists of the systematic study and comparison of relationships among elements of financial information and the investigation of significant. Below are the key inventory assertions that are necessary for the course of the audit.

Audit of Purchases Vouching cash and credit purchases Forward purchases Purchase returns. This is the risk that an auditor will express an inappropriate audit opinion on the entitys compliance and on the documents under review. For example assertions in respect of an item appearing in the balance sheet to be verified may be remembered as VCREP in the mnemonic form wherein V stands for Valuation C stands for completeness.

Assertions about classes of transactions and events for the period under audit. According to the international accounting standards and generally accepted accounting principles every entity is supposed to prepare annual financial statements including the following. ISA 500 Audit Evidence.

My response to higher risk assessments is to perform certain substantive procedures. B for most assertions analytical procedures are considered to be more effective than tests of details. Among other things the SAS provides guidance in AU-C section 501 Audit Evidence Specific Considerations for Selected Items on applying SAS No.

Having a good audit software package could not only improve the effectiveness of our audit review but would also help us to save time by allowing the computer to do some of the work for us. In an attestation review the client makes specific assertions. As auditors we usually audit inventory by testing the various audit assertions including existence completeness rights and obligations and valuation.

I and II only c. The overall objective of an auditor in terms of gathering evidence is described in audit standards namely. The assertions listed in ISA 315 Revised 2019 are as follows.

Namely a search for unrecorded liabilities and detailed expense analyses. Plant property and equipment is often the largest item on a balance sheet. The audit of payables places more emphasis on collecting evidence about the completeness assertion relative to the E or O assertion.

Purchases and cash. This would also be a very time consuming process. Balance confirmation from broker company in respect of securities held.

Assertions used by the auditor fall into the following categories. In the United States information about individuals video purchases is protected--the result of one unfortunate experience by one legislator. Adds a new appendix to AU-C.

Review notes pertaining to questions and comments regarding the audit work performed. There are various assertions and the relevant objectives of each assertion that the auditor can carry out to test the inventory during the course of the audit. In audit Analytical Procedures that seek to provide evidence as to the completeness accuracy and validity of the information contained in the accounting records or in the financial statements.

The objective of the auditor is to design and perform audit procedures in such a way to enable the auditor to obtain sufficient appropriate audit evidence to be able to draw reasonable conclusions on which to base the auditors opinion. The permanent file section of the working papers that is kept for each audit client most likely contains. Analytical Procedures in Audit.

An audit may help a site to convince consumers of its good information practices and to distinguish it from. AR The allowable audit risk that monetary misstatements equal to tolerable misstatement might remain undetected for the account balance or class of transactions and related assertions after the auditor has completed all audit procedures deemed necessary. Assertions about presentation and disclosure.

Perform analytical procedures on purchases returns comparing the purchase returns as a of sales or cost of sales to the previous year. Inspecting the investments that are tangible physically. Assertions relating to presentation and disclosure classification and understandability.

Income statement Balance sheet Statement of changes in equity Statement of cash flow These statements or reports are made in order to provide a clear understanding of how the business. II and III only d. And the accounting is usually not difficult.

Overview of property plant and equipment.

Auditing Accounts Payable And Expenses A Guide Cpa Hall Talk

Procedures For Student Directional Testing Online Presentation

Audit Expenses Assertions Risks Procedures Accountinguide

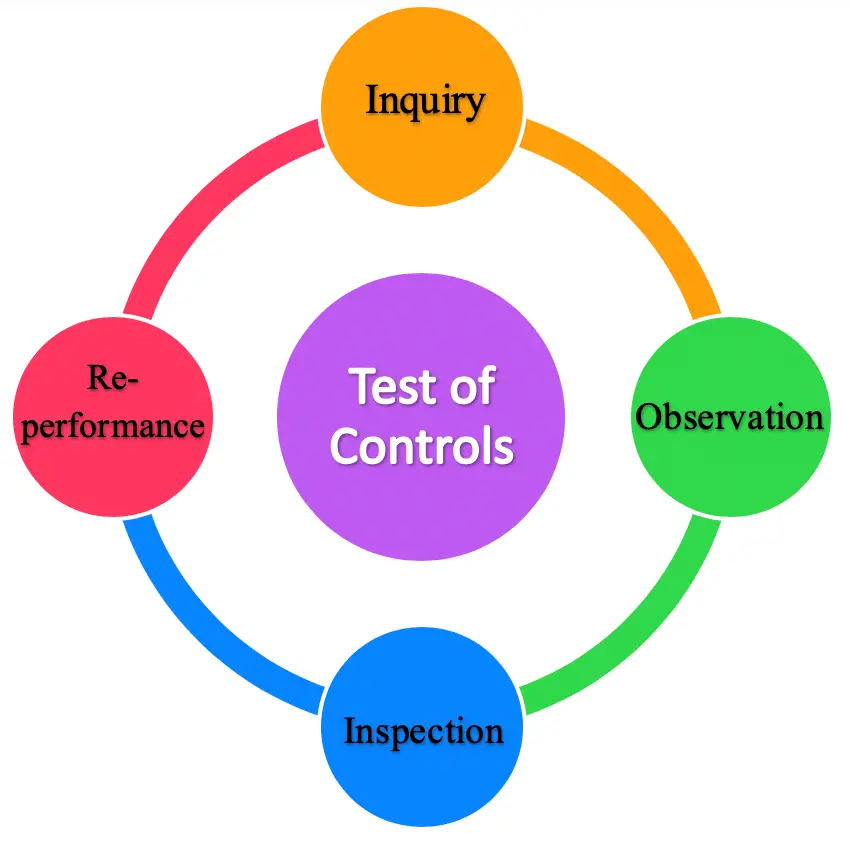

Test Of Controls Purposes Types Vs Test Of Details Accountinguide

Financial Statement Assertions Auditors Can Use A Framework Built Around Five Types Of Assertions To Help Assure Financial Statements Are Fairly Presented Document Gale Academic Onefile

Chapter 9 Audit Procedures

Assertions About Classes Of Transactions Events For The Period Youtube

Substantive Tests